Pull a restaurant card processing statement off the desk of any ten independents and the same thing will happen ten times. The owner will glance at the front page, point at the headline rate (usually something like 2.65% or 2.9% + 10c), and tell you that is what they pay. Then you do the actual division - total fees on the last page divided by total card volume - and the real number comes out 30 to 90 basis points higher than the headline. Sometimes much higher. The gap between the rate on the front page and the effective rate that actually lands on the P&L is the entire game in restaurant payments, and almost nobody is taught to look at it.

This guide is the operator's playbook for closing that gap. It covers the three pricing models you will see in any quote (interchange+, flat-rate, and tiered), the three cost layers that make up your statement (interchange, assessments, processor markup), the seven hidden fees that operators routinely miss, how the card mix at your specific venue type pushes your costs up or down, the 2026 regulatory backdrop that is reshaping rates this year, a straight script for negotiating with your current processor, and the honest signals for when to switch. Embedded in the middle is a free Effective Rate Calculator that takes the information off page one of your statement and turns it into the number that actually matters. By the end you should be able to benchmark your current pricing in under 10 minutes and know whether you have $2,000, $20,000 or $80,000 a year sitting on the table.

Why payments is the second-largest variable cost you ignore

The first lesson on any independent owner's first day is that food cost and labour cost together form prime cost, and prime cost is the number you have to manage every week if you want to make rent. Both numbers get a weekly review, sometimes a daily one. Inventory counts. Schedule edits. Recipe re-specs. Hours of attention every month from the GM and the chef.

Card processing is the third-largest variable line on most casual full-service P&Ls. A venue doing $1.6M a year with 80% card volume pays roughly $1.28M through the terminal, and at a typical 2.7% effective rate that is $34,560 a year in processing fees. Pull the effective rate from 2.7% down to 2.2% by renegotiating the markup, and the same restaurant keeps $6,400 a year - more than a one-point cut in food cost would deliver on the same revenue base. Get it down to 1.9%, which is realistic for a healthy prime-cost business at that volume on a properly priced interchange+ plan, and the savings cross $10,000. And the saved dollars are clean: no supplier renegotiation, no payroll fight, no recipe rewrite, no service compromise. You just have to read the statement.

The reason almost every operator under-attends to this line is that the statement is deliberately impossible to read. It is the one piece of paper in restaurant operations that is designed to be ignored, and it works. The vendor sends a 12-page PDF every month with 80 line items, batched and unbatched fee summaries, "qualified" and "non-qualified" surcharges, and a "total fees" number on page 11 that hardly anyone divides into the volume number on page 1. The processor's commercial model depends on you not doing that division. Once you do, the conversation changes.

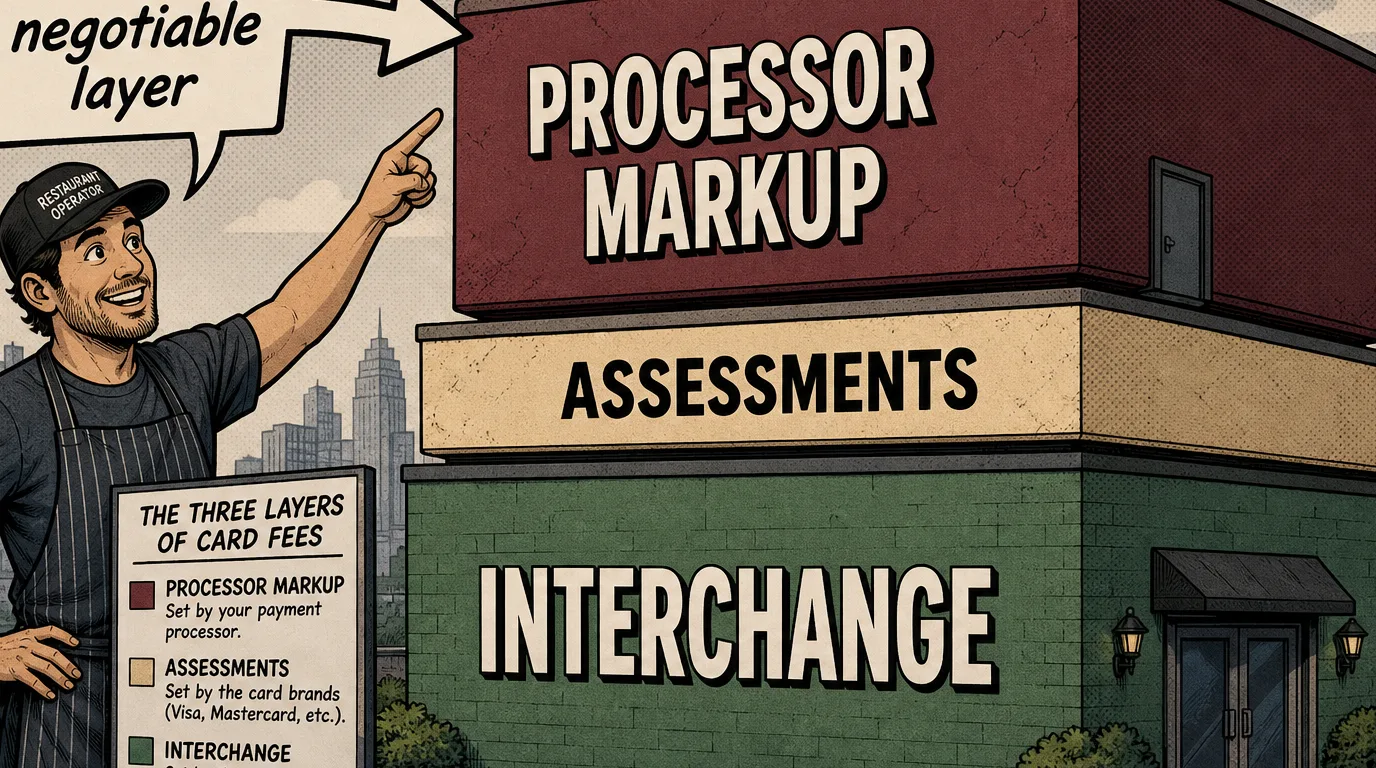

The three layers behind every dollar you pay

Every card payment fee you ever pay - regardless of who your processor is, what hardware you use, or which pricing model you sit on - is built from three stacked layers. Understanding the layers is the prerequisite for everything else, because each layer is set by a different party with different leverage, and where you can negotiate depends entirely on which layer you are looking at.

Layer one is interchange. This is the fee paid to the bank that issued the customer's card (the issuing bank), and it is set by the card networks - Visa, Mastercard, American Express, Discover. Interchange is published, public, updated twice a year (April and October), and there are roughly 300 different interchange categories depending on card type, transaction environment (in person vs. card-not-present), and merchant category. For a card- present, swiped/dipped/tapped transaction at a US restaurant in 2026, interchange runs from about 0.45% + 15c for a regulated debit card up to 2.50% + 15c for an American Express premium rewards card. Interchange is not negotiable. Every processor pays the same interchange to the issuing bank. If a salesperson tells you they can get you "lower interchange" they are either confused or lying.

Layer two is assessments. These are the fees paid to the card networks themselves for the use of their rails. Visa and Mastercard each charge about 14 basis points of volume as their assessment, plus a small per-transaction fee (called the "Network Access and Brand Usage" fee, NABU on Mastercard, APF on Visa, currently around 2c per authorisation). American Express charges a higher network fee but bundles it differently. Like interchange, assessments are not negotiable. They are the same for every processor.

Layer three is the processor markup. This is the only layer the processor actually controls and the only layer where negotiation lives. The markup is whatever your processor adds on top of interchange and assessments to make a margin. On an interchange+ plan the markup is explicit and quoted as "X basis points + Y cents per transaction" - say 30 bps + 10c. On a flat-rate plan (Square, Stripe, Toast Flex, Clover Go) the markup is hidden inside the single all-in rate: when you pay 2.6% + 10c at Square, roughly 1.6-2.0% of that is interchange + assessments and the rest is Square's margin, which fluctuates with the card mix you actually take. On a tiered plan the markup is hidden inside the qualified / mid-qualified / non-qualified bucket assignments.

The three-layer mental model is the single most useful thing you can carry into a processor conversation. When the salesperson quotes you a rate, the question is always: "of that rate, how much is interchange + assessments, and how much is your markup?" If they will not answer cleanly, the answer is more expensive than you think.

The three pricing models - what each is for

Interchange+ (also called "cost-plus" or "interchange passthrough"). The processor passes interchange + assessments through at cost and charges a fixed markup on top, typically quoted as "X basis points + Y cents per transaction." This is the transparent model and the cheapest plan for any restaurant doing more than about $30,000 a month in card volume. Healthy markups in 2026 for a sub-$100K/month independent run 25-40 bps + 8-12c per transaction; above $100K/month the markup compresses to 15-25 bps + 5-10c. Every dollar you save vs. flat-rate compounds, because the underlying interchange is already as low as it goes.

Flat-rate. A single all-in rate applied regardless of card type. Stripe Restaurant charges 2.7% + 5c in 2026 for in-person, Square charges 2.6% + 10c, Toast Flex starts at 2.49% + 15c. The model is genuinely simpler and the fee per transaction is predictable, which is the real product. For a venue doing under $10,000 a month, the savings on interchange+ usually do not cover the additional account management overhead and flat-rate is the right call. Between $10,000 and $30,000 it is a coin flip that depends on your card mix. Above $30,000 a month, flat-rate is almost always 30-80 bps more expensive than a properly negotiated interchange+ plan.

Tiered (also called "bundled"). The processor sorts every transaction into one of three buckets - qualified, mid-qualified, non-qualified - and charges a different rate per bucket. Headline rate is the "qualified" tier, which usually only applies to regulated debit run in a perfect environment. Real transactions land disproportionately in mid- and non-qualified buckets, where the rates can be 1.5-2.5 percentage points higher. Tiered pricing is the historical default for legacy processors (First Data, Worldpay, Heartland, Elavon) and is almost always the most expensive model. If your current statement uses the words "qualified" and "non-qualified," you are on tiered, and switching to interchange+ alone usually saves 30-100 bps with no other change.

The decision tree is short. Under $10K/month, take flat-rate for simplicity. $10K-$30K, run the effective rate calculator on both options and pick the lower number. Above $30K/month, demand interchange+ from at least three processors and take the lowest markup. If you are on tiered today, get off it. The only operators who should stay on tiered are those who genuinely prefer being overcharged for the comfort of a familiar invoice.

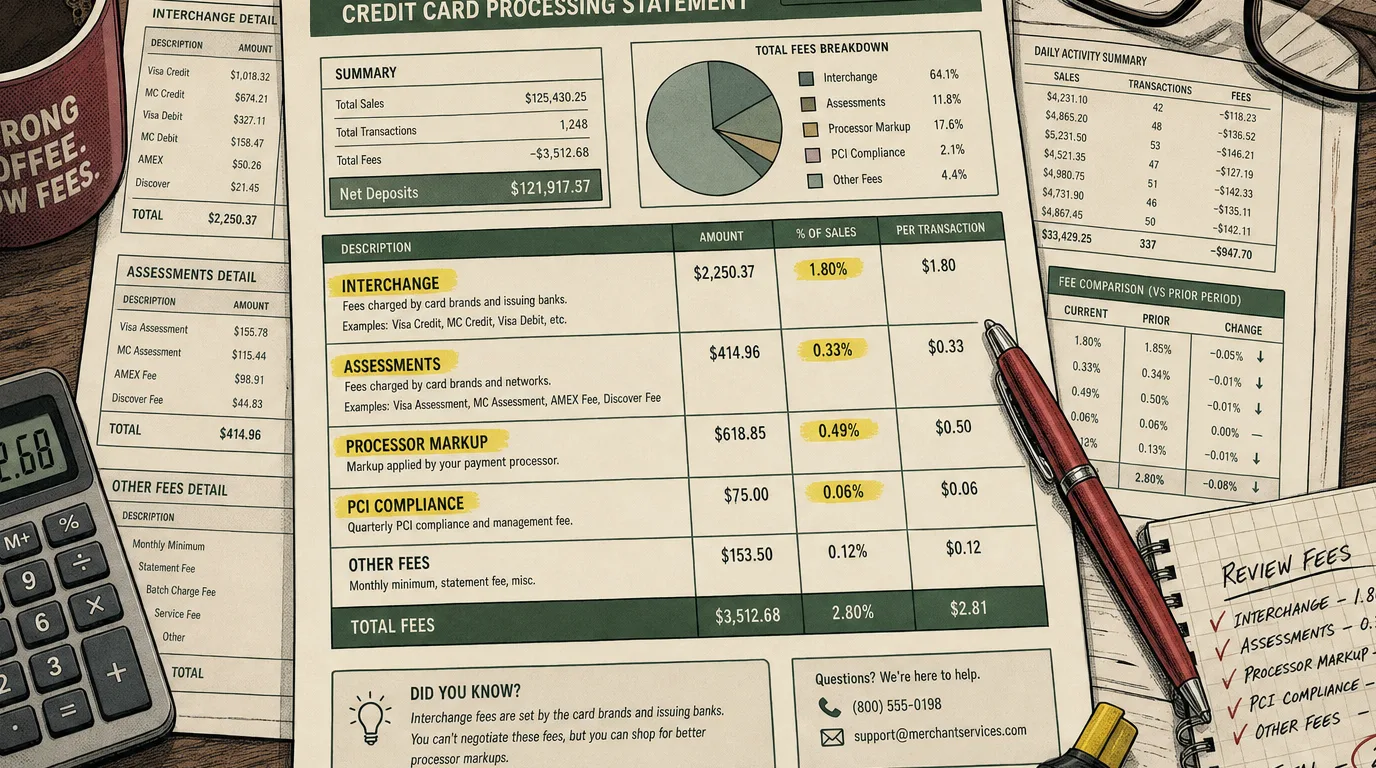

How to read a card processing statement in 10 minutes

The card processing statement is a hostile document, but the structure is consistent across processors once you know what you are looking for. There are exactly five numbers you need, and they are all somewhere on the document - usually on page 1, page 2, the "Fees" summary page and the last page. Pull last month's statement out now and find these five numbers.

1. Total card volume processed. Page 1, almost always at the top. The dollar figure of all card payments processed through the account. Call this V.

2. Total number of transactions. Page 1 or page 2, sometimes in the summary table. The count of card payments. Call this N. Your average ticket is V / N, and that number is the second-most-important input into the effective rate calculator after total volume.

3. Total fees paid for the period. Last page, usually printed in bold as "Total Fees" or "Total Charges." This is the all-in cost of processing for the period - every interchange charge, every assessment, every markup, every monthly fee, every batch fee, every PCI charge, every chargeback fee. Call this F.

4. Your effective rate. F / V, expressed as a percentage. This is the number you want, and it is almost never printed anywhere on the statement. Do the division yourself. For a healthy 2026 restaurant the effective rate should land:

- Under 2.1% - excellent. You are inside the top decile.

- 2.1%-2.5% - good. Healthy independent on interchange+ with reasonable card mix.

- 2.5%-2.9% - average. The industry mean. Real room to renegotiate.

- 2.9%-3.4% - above market. You are paying meaningfully more than you need to. Audit and switch.

- Above 3.4% - predatory. Almost always tiered pricing with aggressive non-qualified surcharges, or a flat-rate plan applied to a high-ticket venue with heavy AmEx mix. Switching processors should pay back inside one month.

5. Sum of the flat monthly fees. This is the line items that are not a percentage of volume - PCI compliance fee (typically $15-$25/month), statement fee ($5-$15), gateway fee ($10-$30), monthly minimum ($25-$50), batch fee ($0.25 per batch times ~30), tokenisation fee, IRS reporting fee (1099-K), and so on. Sum them up. On a healthy account these add up to under $50/month. On a legacy tiered account they routinely add up to $200/month or more, which on a $40K/month volume venue is another 50 basis points of effective rate before you even start counting per-transaction charges.

Now plug those four numbers (V, average ticket V/N, your current rate structure, the sum of flat fees) into the calculator below and the rest of the diagnosis writes itself.

The seven hidden fees most operators miss

The headline rate is the small print of payments. The fees that actually move the effective rate live below the fold, scattered across the statement under names designed to look administrative. A walk through the seven that show up most often, in roughly the order they bleed independents.

1. PCI non-compliance fee. Every processor requires you to complete a Payment Card Industry Self-Assessment Questionnaire (SAQ) annually. Forgetting to file the SAQ triggers a "PCI non-compliance fee" of $20-$40 per month, every month, until you complete it. The fee is invented; the processor pays nothing extra for your non-compliance. The fix is to renew the SAQ once a year. The fee is pure rent on operator inattention.

2. PCI compliance fee. Yes, also a fee for being compliant. Typically $10-$25/month. Some processors charge both: you pay PCI compliance every month, plus a non-compliance surcharge if your SAQ lapses. Both fees are mostly negotiable. On a healthy independent contract this line is $7-$15/month; if your statement shows $30+/month for PCI alone, call and ask for a discount.

3. Monthly minimum. "If your fees do not reach $25 this month, we charge you the difference up to $25." For a restaurant doing any real volume this rarely triggers, but in the slow weeks of January or August it can quietly add a line. The monthly minimum should be waived on contract for any venue doing more than $5K/month volume; if it is not, ask.

4. Statement and reporting fees. $5-$15/month for receiving the statement. Some processors charge $5 extra for emailed PDFs vs. mailed paper. These are 100% margin for the processor and 100% negotiable.

5. Batch fee. $0.10-$0.30 per batch close. Closing the batch is the end-of-day reconciliation step in your POS. At 30 batches a month and 30c per batch, that is another $9/month - small but pure markup. Negotiable on volume contracts.

6. Voice authorisation fee. Charged when a card has to be authorised by phone (rare in 2026 except for AmEx high- limit cards in card-not-present situations). $0.65 - $2.00 per event. If you see this fee at all and you are not a high-end venue, your terminal config is probably routing transactions through a fallback channel that should be fixed.

7. Chargeback fee. $15-$35 per disputed transaction, charged whether you win or lose the dispute. This one is legitimate (chargeback handling has real cost) but the fee is usually negotiable down to $15. If you have more than two chargebacks a month you have a guest communication problem upstream and should also tighten your refund policy at the till.

Cumulatively these seven items add 15-60 basis points to the effective rate without ever touching the headline. They are also the fastest part of the contract to fix: a 20-minute phone call asking your account manager to "review the maintenance fees" routinely shaves $40-$100/month off a small independent's bill.

Why card mix matters - and why a wine bar pays more

Interchange is not a single number. It is roughly 300 numbers, varying by card type, transaction environment and merchant category. The mix of card types your specific venue takes is the second biggest driver of your effective rate after your pricing model. Two restaurants on the exact same interchange+ contract with the exact same markup can have effective rates 50 basis points apart simply because of who their guests are and what is in their wallets.

The cheap card to take is a regulated debit card. Under the Durbin Amendment in the US, debit cards issued by banks with more than $10B in assets are capped at 0.05% + 22c interchange. A $40 average-ticket restaurant taking 60% debit pays roughly 35-50 basis points blended interchange on that 60% of volume. The expensive cards to take are premium rewards credit cards (Chase Sapphire Reserve, Amex Platinum, Capital One Venture X) which carry interchange around 2.10%-2.40% + 10c, because the issuing bank uses that interchange to fund the points and miles the cardholder redeems. The most expensive is a high-limit American Express card, which can hit 2.70%+ depending on the program.

This is why the card mix at a fast-casual taco shop costs the operator a different amount per dollar than the same dollar at a Michelin-starred tasting menu. The taco shop takes mostly debit on small tickets ($14 average), heavy contactless and Apple Pay (which routes as debit when the customer has a debit card linked) and the blended interchange comes in around 1.0%. The tasting menu takes mostly premium credit cards on large tickets ($240 average) with heavy AmEx mix, and the blended interchange comes in closer to 2.2%. Same processor, same contract, very different bottom-line effective rate.

Three practical implications. First, when you are benchmarking, compare yourself to your format peers, not the industry mean - a 2.4% effective rate is exceptional for a wine bar and disappointing for a QSR. Second, the more debit you can encourage (PIN entry prompts, debit-friendly checkout flow, no "credit only" hardware quirks) the lower your blended interchange will be at the same processor. Third, if you do not accept AmEx today, the question is not "should we accept AmEx" - it is "does the basket-size lift from accepting AmEx (typically 5-10% on premium concepts) more than cover the 50-80 bps higher cost?" At fine dining and steakhouses the answer is almost always yes. At a $14 average-ticket cafe, almost always no.

Surcharging, cash discounts and the 2026 regulatory backdrop

The conversation around restaurant payment fees in 2026 is shaped by two simultaneous trends pulling in opposite directions. Card networks are pushing interchange up; regulators and merchants are pushing back. The net effect on your statement depends entirely on which jurisdiction you operate in and which choices you make.

In the US, both Visa and Mastercard implemented interchange increases on regulated and unregulated cards in April 2026, the largest set of changes since the 2018 rebanding. The headline impact on restaurants is that mid-volume credit card interchange went up roughly 5-10 basis points across most categories, partially offset by some debit category reductions. If your processor passes interchange through (interchange+) you saw the change in your statement within two months. If you are on flat-rate, you saw nothing - the processor absorbed the change, but they may renegotiate your contract at renewal to recover it.

On the merchant side, surcharging - the practice of adding a small surcharge (typically 2-4%) to credit card payments to recover processing costs - is now permitted in 46 US states and Canada, with state-specific rules on disclosure, cap (most states cap at 3% or the cost of acceptance), and whether you can surcharge debit (no, ever - debit surcharging is prohibited everywhere). In 2026 Visa and Mastercard updated their surcharging rules to require a new merchant registration and clearer point-of-sale disclosure. Done correctly, surcharging shifts roughly 70-80% of the processing cost to the guest, with a small (1-3%) reduction in card volume as some guests switch to cash or debit. Done incorrectly (no signage, no register prompt, debit surcharged accidentally) it triggers card network fines and customer complaints. The decision is heavily format-dependent: it works for QSR and counter service where the checkout flow surfaces the fee naturally; it is much harder for full-service where the guest does not see the bill until the meal is already over.

The cash-discount alternative is functionally similar but structured as a discount off a "card-priced" menu when the guest pays cash. The math is identical but the customer-facing framing is different. Cash discount is permitted in all 50 states with no network registration required, which is why many independents prefer it.

In the EU, the Interchange Fee Regulation (IFR) caps consumer card interchange at 0.20% for debit and 0.30% for credit, which is why a Berlin or Paris restaurant typically sees effective rates 80- 120 basis points lower than its NYC equivalent. Surcharging on EU- issued cards is prohibited under PSD2; commercial cards (not consumer cards) are exempt from the IFR cap and routinely run 1.5- 2.0% interchange, which is why hotel restaurants and business-lunch concepts in EU capitals can still see surprising fees on AmEx business cards.

How to negotiate with your processor - a script

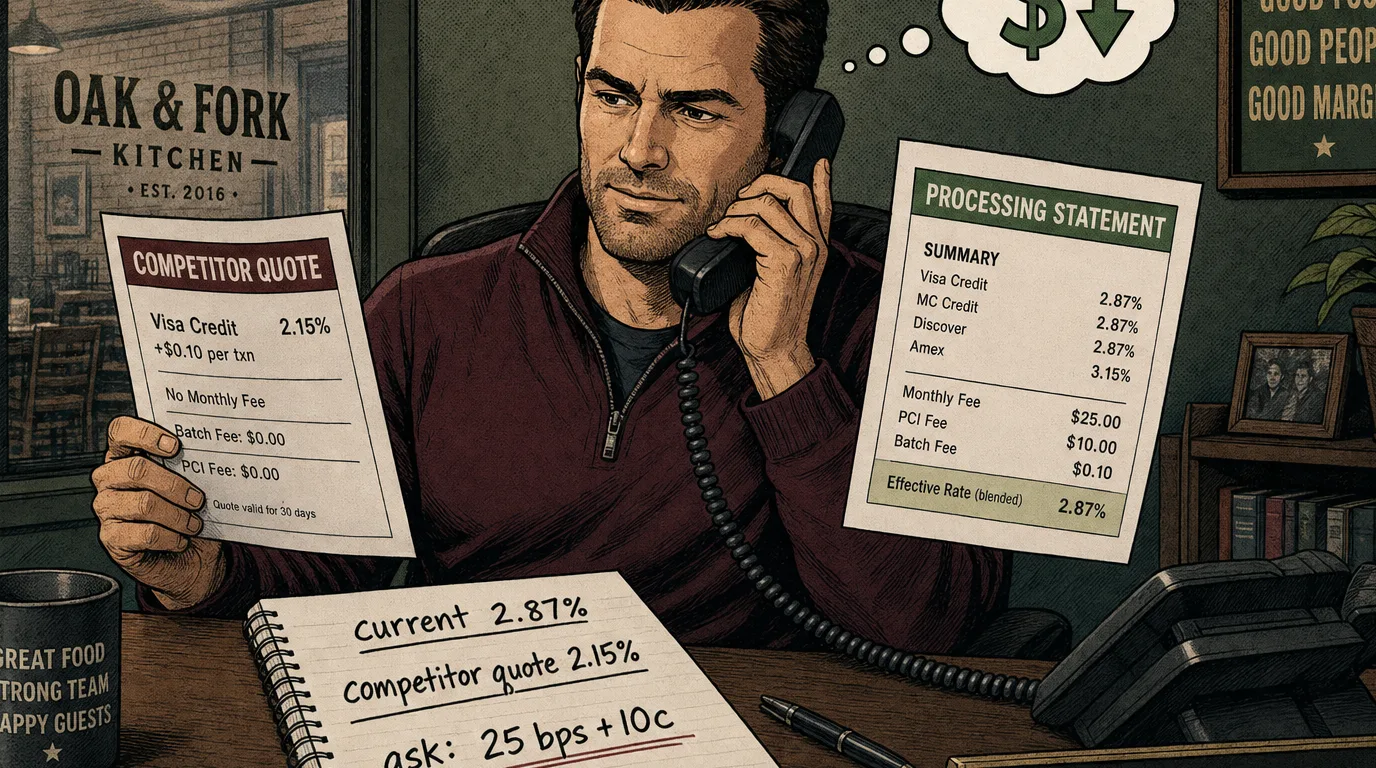

The single most under-used lever in restaurant payments is the renewal conversation. Most processor contracts auto-renew on the anniversary with no notification and a quiet rate adjustment upward; most operators never read the renewal terms; processors know this and price accordingly. A 25-minute phone call once a year is worth more dollars per minute than almost anything else the owner does in the month. The script below is the one that works most often on a healthy independent account.

Step 1: gather evidence. Pull the last three months of statements, run the calculator on each, write down the effective rate for each month and the average. Identify the three highest line-item fees on the most recent statement and write down what they are. Sum the monthly flat fees and write that number down. Write down your total card volume for the trailing 12 months.

Step 2: get two competitive quotes. Contact two other processors - one large (Fiserv, Worldpay, Global Payments, Adyen, Stripe) and one independent or restaurant-specialist. Tell them your trailing 12-month volume and average ticket and ask for an interchange+ quote with a flat markup. Get the quote in writing including the markup, per-transaction fee, monthly fees, contract term and termination clause. Most processors will quote within 48 hours if they think the account is winnable.

Step 3: call the incumbent. Ask for your dedicated account manager (not the support line). Open with: "I am auditing our processing costs. Our effective rate over the last three months is X.X%. We have a quote from [competitor] for interchange+ at Y bps + Zc with [list of waived fees]. Before we switch I want to give you the chance to match or beat." Then stop talking. The silence does the work.

Step 4: what to ask for, in order. Move to interchange+ pricing if you are not on it. Markup compressed to match or beat the competitive quote. PCI compliance fee reduced or waived. Monthly minimum waived. Statement fee waived. Batch fee reduced. Terminal lease eliminated (or buy out the lease and own the hardware). Three-year contract reduced to month-to-month with no early termination fee.

Step 5: what they will offer. A small markup reduction (10-15 bps) without changing model. A "PCI fee credit" for six months. A one-time "loyalty bonus" credit on next month's statement. Reject the one-time credits and push on the structural fix: markup compression and monthly fee removal. Structural changes compound; one-time credits are theatre.

Step 6: walk away. If after 15 minutes you do not have a structural improvement that brings your projected effective rate within 15 bps of the competitive quote, accept the competitive quote. Switching processors is operationally straightforward in 2026 - most quotes include a "switch concierge" who handles the terminal swap, the POS integration update, and the closing of the old account. The downtime risk used to be real; with modern cloud POS it is usually under an hour.

Your POS and the economics of payments

The single biggest hidden variable in your processing economics in 2026 is the relationship between your POS and your processor. There are three structural models, and each one produces a different rate dynamic.

Bundled - POS sells payments at a fixed flat rate. Square, Clover, Toast Flex. The POS and the payment processor are the same company. The headline rate is simple. The economics are captive: you cannot change processor without changing POS. For a small independent doing <$15K/month this is genuinely the right trade-off - the bundling overhead is below the savings you would get from unbundling. For a venue doing $40K+/month the bundled rate is almost always 50-100 bps more expensive than what you could get on an unbundled stack.

Integrated - POS supports multiple processors via a certified payments integration. Tableview's POS, Lightspeed, Square (sort of, through their unique integration program), most enterprise POS systems. You pick the processor independently of the POS, and the integration handles the terminal, the receipt printing, the tip flow, the open-tab adjustments, the tip-out at end of shift. This is the structure that gives you the most leverage - you can shop the payments quote on its own merits, switch processors without changing POS, and benchmark your rate against the market every year. Tableview Payments runs as either an integrated processor or a bring-your-own setup depending on what makes more sense for the venue's volume and mix.

Gateway-only - POS sends transactions through a separate gateway that connects to any processor. Legacy enterprise setups. Maximum flexibility, maximum technical complexity, usually the wrong choice for an independent. Almost no new independents deploy a gateway-only architecture in 2026 unless they have a specialist payments team.

The practical recommendation is integrated. The single processor relationship at the bundled vendor produces a rate ceiling you cannot beat without unbundling, and gateway-only adds an operational layer that is rarely worth the marginal flexibility. Tableview's POS supports both an integrated Tableview Payments configuration and bring-your-own processor for operators who want to keep an existing relationship.

A 30-day audit and savings plan

The action plan that converts everything above into actual dollars on the bank account. Block four 90-minute sessions across 30 days. By day 30, an operator on a typical independent contract should have shaved 25-60 basis points off the effective rate, which on a $1.6M restaurant is $3,200-$7,700 a year of recurring savings. On a multi-unit operation the numbers scale linearly.

Week 1 - audit. Pull last three months of statements. Run them through the effective rate calculator and document the trend. Identify which pricing model you are currently on (interchange+, flat, tiered). List every flat fee on the most recent statement and what each one is. Calculate your current cost per transaction. Note any month-over-month rate drift.

Week 2 - benchmark. Request interchange+ quotes from two competing processors with your trailing 12-month volume. While you are waiting for the quotes, run the same calculation yourself: at your volume and card mix, what would interchange+ at 25 bps + 10c cost you? That is your floor benchmark. Look up the network interchange tables for your typical card mix and confirm the benchmark.

Week 3 - negotiate. Run the script above with your incumbent account manager. Capture every promise in writing (email follow-up the same day). If the structural offer lands within 15 bps of the floor benchmark, accept and move on. If it does not, take the better of the two competitive quotes and start the switch process.

Week 4 - re-baseline. Whether you renegotiated or switched, the new pricing takes effect 1-2 statement cycles later. Calendar a follow-up audit in 60 days to verify the new rates are what was agreed. Set a recurring annual reminder to repeat the full audit. The mistake is treating the negotiation as a one-time event - rates drift up quietly, and the savings need to be re-earned every year.

The conversation about payments rarely produces drama. Nobody quits, nothing breaks, no guest notices. But on a healthy independent the recurring savings compound across years and free up the same kind of capital that a full break-even analysis usually surfaces - except this one does not require any operational change at all. It just requires you to read the statement, do the division, and have the 25-minute conversation. Pull the statement now.

The bottom line

Restaurant payment processing is the line on the P&L where the smallest amount of operator attention produces the largest amount of money kept. The asymmetry is structural: processors price to inattention, statements are designed to be ignored, and the effective rate that actually lands on the bank account is almost never the rate on page one. Once an operator learns to do the single most important calculation - total fees divided by total volume - the rest of the playbook is mostly courage. Pick the right pricing model for your volume. Negotiate the markup once a year. Audit the seven hidden fees. Match your hardware and POS to your processor strategy, not the other way around. Use the Effective Rate Calculator to test every quote before you sign. The rest of the calculator hub sits next to it for the adjacent decisions - P&L planning, food cost benchmarking, marketplace margin when the third-party channel pulls in volume with its own processing economics, and lifetime value when the loyalty program is the real reason you are absorbing premium card costs.

The bigger picture is that payments is one of the few line items where the operator's leverage is high, the technical complexity is contained, and the savings are recurring. Spend the half day. Do the math. Have the call. Tableview's job is to make the surrounding stack - POS, mobile ordering, Payments - work together so the savings you find here do not get reabsorbed by operational friction elsewhere. The single decision that compounds hardest in 2026 is treating payments as a managed cost line, not as a fixed utility bill.